In an age where supply chains are battlegrounds and energy transitions double as defense imperatives, the quest for raw material sovereignty has never been more urgent. Enter Leading Edge Materials, a Canadian-headquartered mining explorer whose European-centric portfolio positions it as a linchpin in the continent's bid to wean itself off Chinese dominance in critical minerals. On a recent podcast we hosted CEO Kurt Budge, and he laid bare the company's strategic playbook, painting a vivid picture of opportunity amid volatility and covered the assets spanning heavy rare earth elements (HREE), graphite, and polymetallics,

As Europe grapples with export curbs from Beijing, surging demand for electric vehicle (EV) batteries, and escalating military needs, Budge's conversation underscored a "once-in-a-lifetime generational opportunity." This isn't hyperbole; it's a calculated bet on assets that could redefine Europe's industrial resilience. Drawing from Budge's insights, this article dissects Leading Edge's portfolio, the macroeconomic forces at play, and the milestones that could propel the company from junior explorer to strategic powerhouse.

Listed on the TSX Venture Exchange in Toronto and the Nasdaq First North in Stockholm—with OTCQX and Frankfurt listings for broader reach—Leading Edge Materials operates exclusively within the European Union, a deliberate choice that sidesteps the regulatory thickets of more exotic jurisdictions. "We have a portfolio of critical raw materials projects all located in the EU," Budge explained, highlighting three flagship assets that form a diversified triad: immediate-impact rare earths, near-term graphite production, and exploratory upside in base and battery metals.

At the core is Norra Kärr in Sweden, a HREE project that Budge describes as "relatively unique in European terms." Discovered by the Swedish Geological Survey in the early 20th century and later designated a "national interest" for its mineral significance, Norra Kärr boasts one of the continent's largest and most advanced HREE deposits. It's not just about scale; the site's geology yields dysprosium and terbium—elements pivotal for high-performance permanent magnets used in EV motors and defense technologies like missile guidance systems.

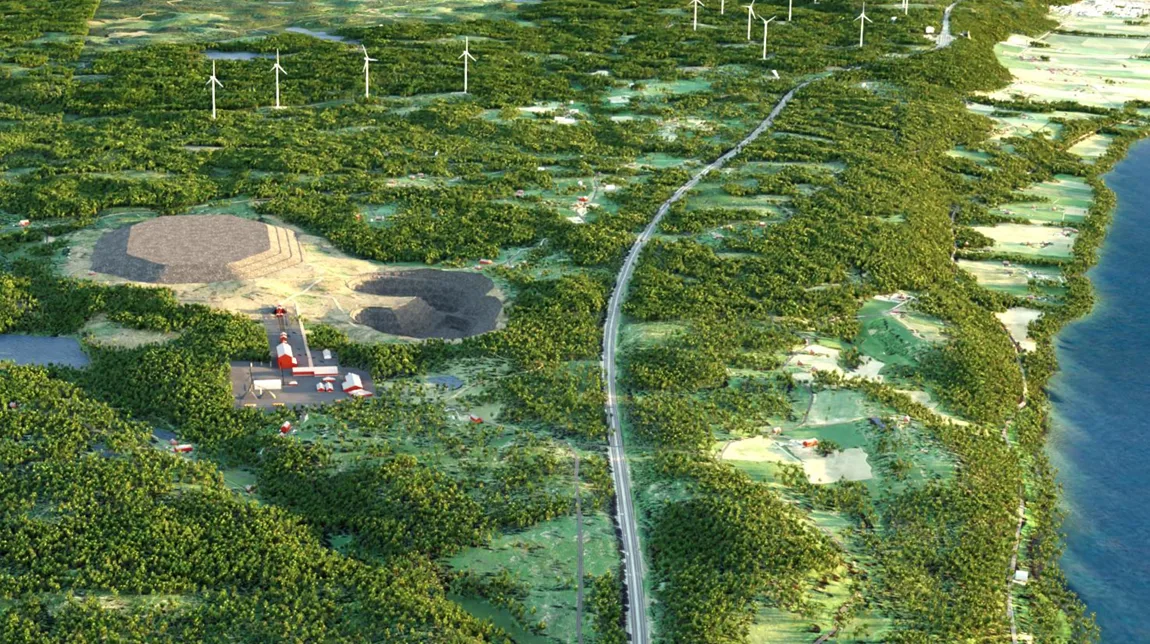

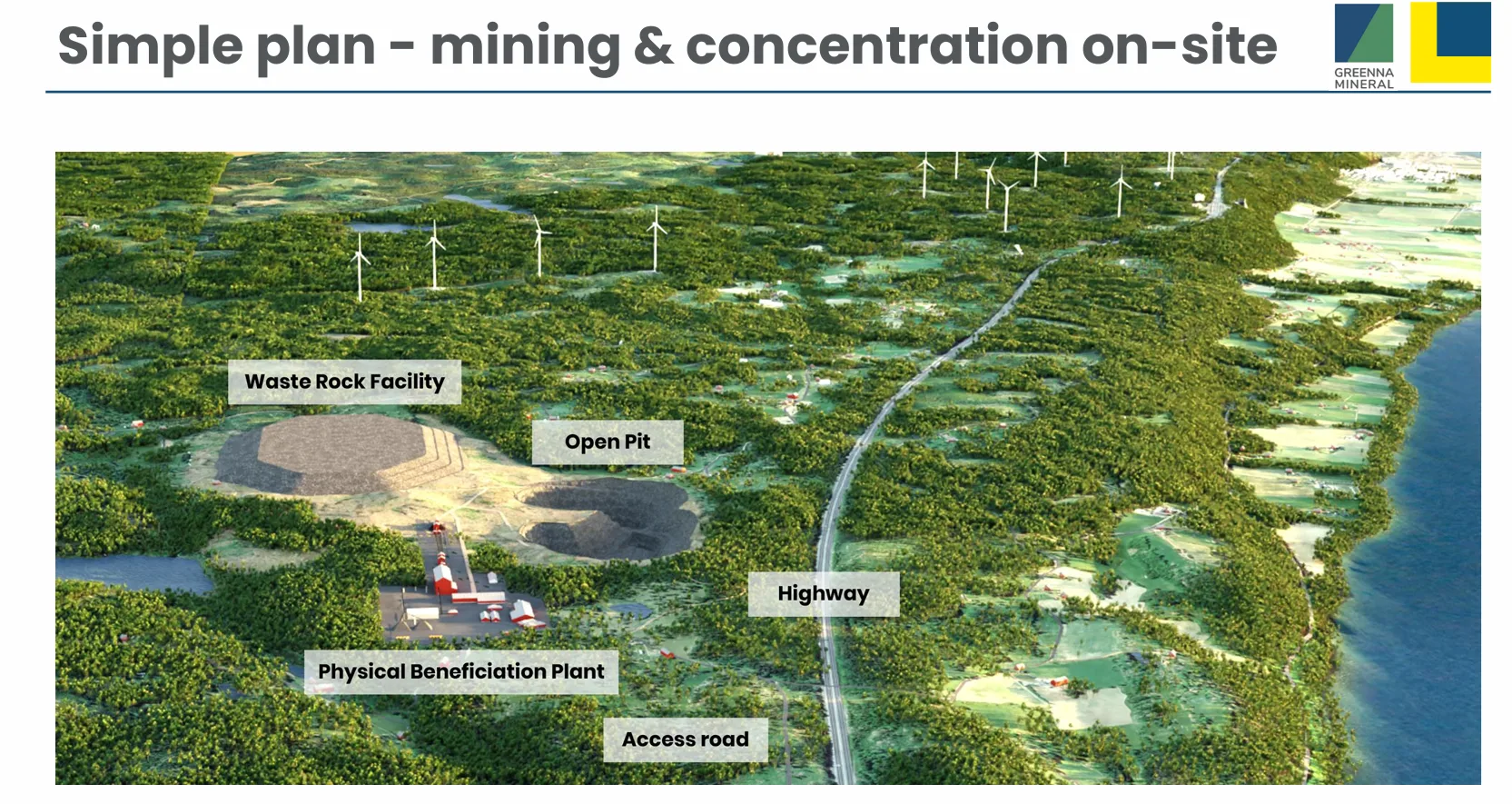

Complementing this is Woxna, an idled graphite mine in central Sweden, primed for revival as a "near-term cashflow generator." With existing infrastructure, permits, and a proven resource, Woxna stands ready to supply flake graphite, a cornerstone of lithium-ion battery anodes. Finally, the Bihor Sud exploration alliance in Romania taps into the prolific Tethyan Metallogenic Belt, targeting a polymetallic bounty: nickel, cobalt, lead, zinc, and copper. This brownfield site—replete with legacy underground workings—offers diversification into battery metals and base commodities, albeit on a longer timeline.

This EU-exclusive footprint isn't coincidental. Sweden's mining-friendly regime and Romania's untapped potential provide a stable base, while proximity to end-markets minimizes logistical risks. As Budge noted, "Sweden is a tremendous jurisdiction for developing mining assets," underscoring a portfolio engineered for strategic autonomy rather than speculative glamour.

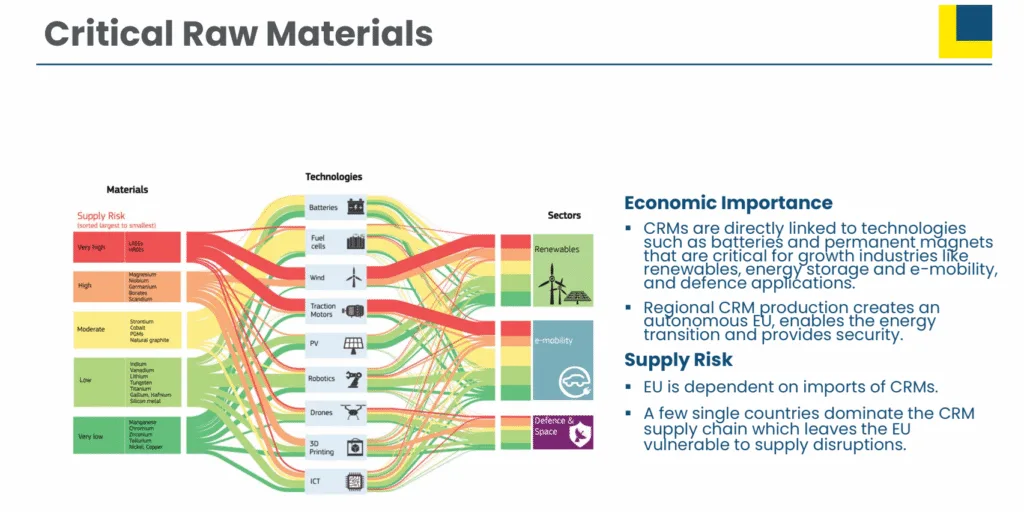

The interview's fulcrum was geopolitics, where "uncertainty is the new norm." Budge framed the current landscape as a convergence of the energy transition and defense industrialization—a "spotlight" on assets like Norra Kärr and Woxna. China's April 2025 export restrictions on rare earths, though partially relaxed in July following EU negotiations, sent "shockwaves through the supply chain." Prices for dysprosium and terbium spiked, exposing Europe's 98% reliance on Chinese HREE and igniting volatility that "isn't going to go away."

This weaponization of trade dovetails with the EU's Critical Raw Materials Act (CRMA), enacted in 2024 to mandate secure, diversified supply chains. By 2030, Benchmark Mineral Intelligence forecasts a 140% surge in graphite demand, necessitating dozens of new mines globally. Yet, with China controlling 80% of refined graphite, the EU faces a stark shortfall. Woxna, with its "established mine... infrastructure and permits," emerges as a ready antidote, appealing to manufacturers seeking "non-Chinese flake graphite production."

Budge's optimism is data-driven: Norra Kärr's HREE profile aligns with permanent magnet needs for EVs (projected to claim 30% of global vehicle sales by 2030) and defense (e.g., F-35 jets and drones). "Our project portfolio is front of mind," he asserted, as NATO's rearmament and the U.S. Inflation Reduction Act's incentives pull allies toward non-Chinese sourcing. In this dual-use paradigm, Leading Edge's assets transcend commodities—they're geopolitical chess pieces.

If Leading Edge has a North Star, it's Norra Kärr. "My focus and the company's focus is very much first and foremost on Norra Kärr," Budge declared, citing its potential as a "transformational" value driver. This isn't mere rhetoric; the project has accrued 15 years of technical de-risking, including a 2015 pre-feasibility study (PFS) that validated economic viability.

If Leading Edge has a North Star, it's Norra Kärr. "My focus and the company's focus is very much first and foremost on Norra Kärr," Budge declared, citing its potential as a "transformational" value driver. This isn't mere rhetoric; the project has accrued 15 years of technical de-risking, including a 2015 pre-feasibility study (PFS) that validated economic viability.

What elevates Norra Kärr? Its geology: a carbonatite-hosted deposit rich in HREE, plus byproduct industrial minerals like nepheline syenite—a feldspar derivative prized for glass, ceramics, and construction. The 2021 preliminary economic assessment (PEA) quantified this synergy, projecting enhanced economics from nepheline sales that could "boost the economics of Norra Kärr" beyond REE alone. At full tilt, the mine could yield 5,000-6,000 tonnes of rare earth oxide annually, with a mine life exceeding 20 years.

Progress is methodical. In 2025, Leading Edge submitted supplementary data for a mining lease, eyeing a decision by year-end—"the Christmas present that I want." Parallel PFS workstreams refine capex and opex, building on 2015's foundation. Yet, the real accelerant is the CRMA's strategic project designation. After missing the initial 47-project list, Budge is undeterred: "We will [reapply]... we've got to join up the dots with the feedback we got from the EU." The January 2026 deadline looms, promising fast-tracked permitting and financing access. As Budge quipped, with an asset "part of the European conversation... for more than a decade," rejection feels like an anomaly, not a verdict.

For Europe, Norra Kärr's importance is existential. HREE scarcity hampers green tech ambitions; a domestic source could cut import risks by 20-30% for key alloys. Budge's pitch: It's not just a mine—it's a bulwark against supply shocks.

While Norra Kärr commands the long game, Woxna offers tactical wins. Idled since 2005, the mine's 2022 restart study provided a blueprint, but 2025's rethink incorporates "innovations... in the last 20 odd years." Testwork underway targets "high quality flake graphite concentrate," with results feeding a revised business case by year-end.

While Norra Kärr commands the long game, Woxna offers tactical wins. Idled since 2005, the mine's 2022 restart study provided a blueprint, but 2025's rethink incorporates "innovations... in the last 20 odd years." Testwork underway targets "high quality flake graphite concentrate," with results feeding a revised business case by year-end.

Demand-side momentum is palpable: "The supply chain [is] coming to us," Budge revealed, as battery makers diversify from China amid U.S. tariffs and EU carbon border adjustments. Woxna's +25% graphitic carbon resource—totaling 53,000 tonnes indicated—positions it for 20,000-30,000 tonnes annual output, generating €20-30 million in EBITDA at current prices. Critically, it's shovel-ready: rail access, power grid, and environmental permits intact.

Budge envisions collaboration: "The era of collaboration within the European Union... the downstream just wants secure supply." Offtake deals with firms like Northvolt or BASF could fund restarts without dilutive equity, turning Woxna into a bridge to Norra Kärr's ramp-up. In a market where graphite prices hover at $500-600/tonne (up 15% YTD), this asset could deliver first cashflow by 2027, validating Leading Edge's "sustainable plan."

Romania's Bihor Sud alliance tempers the portfolio's urgency with exploration intrigue. Spanning 88 square kilometers in the Tethyan Belt—home to Serbia's Timok and Albania's potential giants—the site blends brownfield efficiency (legacy adits from 1970s mining) with greenfield potential. Targets include nickel-cobalt skarn systems and lead-zinc-copper veins, with 2023 assays hitting 2.5% Ni and 1.8% Co over 5 meters.

Progress has been "slower than envisioned," Budge conceded, prioritizing "safety... regulatory compliance." A summer 2025 operational license for the Avram Iancu area prompted a target reassessment, now crystallized in a competent person's report (CPR)—a NI 43-101 equivalent underway this week. This "comprehensive document" will roadmap drilling and attract partners, easing funding strain. "We've got both battery metals and base metals," Budge emphasized, eyeing nickel-cobalt for EVs and lead-zinc-copper for renewables infrastructure.

Challenges abound: Funding constraints and seismic rehab have paced the program. Yet, the upside glimmers—high-grade hits suggest a multi-metal hub, potentially mirroring Eldorado Gold's nearby Skouries. By Q1 2026, the CPR could unlock joint ventures, transforming Bihor Sud from wildcard to workhorse.

Junior miners rarely escape the funding gauntlet, and Leading Edge's August 2025 raise—amid summer doldrums—was no exception. "Probably not the best time... a very tough market for companies that have development projects," Budge admitted, contrasting it with gold's retail allure. Still, the C$2.5 million infusion (via flow-through shares) fuels multi-front advances: Norra Kärr submissions, Woxna tests, and Bihor Sud's CPR.

Budge's candor highlights a broader critique: Europe's CRMA is "great policy," but lacks the U.S./Canadian grant ecosystems. To rival China's "state-sponsored strategies," Budge calls for "avenues for finance... to play a serious game." Milestones like a mining lease or strategic status could catalyze institutional interest, de-risking the equity story. As he put it, "That is transformational... life becomes somewhat easier."

Budge's horizon is milestone-dense: A Norra Kärr mining lease by December 2025; PFS completion in H1 2026; strategic project greenlight post-January; Woxna's business plan and offtake talks by Q4; Bihor Sud CPR in Q1. "There's lots of activity taking place," he said, weaving these into a narrative of de-risking and value creation.

Yet, success hinges on execution and ecosystem support. Europe must match rhetoric with capital—grants, offtakes, tax credits—to bridge the China gap. For investors, Leading Edge offers a rare EU-pure play: HREE scarcity premiums, graphite's supply crunch, and polymetallics' breadth. At a C$15 million market cap, it's undervalued against peers like Mkango Resources (up 50% on REE news) or Northern Graphite (doubled on restarts).

As Budge signed off, wishing "luck with all three fronts," his parting words resonate: In a fluid world, Leading Edge isn't just mining minerals—it's mining Europe's future. For stakeholders from Zagreb to Stockholm, this is a story worth watching. The next move? A mining lease that could unlock the continent's mineral Magna Carta.

Watch the interview with Kurt Budge here

Visit company website here Leading Edge Materials

Disclaimer: Presented company is our client and we are compensated for the creation of this content. This is not a recomendation to buy or sell any shares, products or services, always do your own DD!