This article is made by my friend Stefano from X (@Stefano_1799), a big contributor when it comes to uranium investing thesis. Stefano has already done some excellent analyses of the uranium market and his University Master's Degree thesis is "Advancing into a new nuclear era: the critical role of uranium in global energy dynamics".

This article is made by my friend Stefano from X (@Stefano_1799), a big contributor when it comes to uranium investing thesis. Stefano has already done some excellent analyses of the uranium market and his University Master's Degree thesis is "Advancing into a new nuclear era: the critical role of uranium in global energy dynamics".

Here is his take on Kazatomprom, updated uranium forecast and more.

How Kazatomprom’s policy shift, intertwined with a rising deficit from the 2025 Nuclear Fuel Report results, are are leading the global uranium market into a new stage.

The recent announcement by Kazatomprom—regarding its intention to cut production across 100% of its subsoil use agreements—has sent a clear alarm throughout the uranium market. It represents not just a corporate decision, but a powerful signal directed at utilities and global producers alike: today’s uranium prices fail to capture the real and growing imbalance between supply and demand that will define the next fifteen years, and perhaps even the immediate future.

The magnitude of the planned reduction is striking. By cutting output associated with its subsoil use agreements by 8 million pounds, Kazatomprom effectively triggers a contraction of nearly 10% in its own production and around 5% of total global uranium output. Yet the implications run deeper. The company has also stated its intention to exercise its legal right to further curtail production by up to 20% of its total subsoil agreements—an action that, if realized, could lower 2026 production to just 61.6 million pounds. This would represent a total reduction of 23.4 million pounds—equivalent to a 27% drop from current levels and roughly 15% of global primary uranium supply.

While it is unlikely that the full 20% cut will materialize, the announcement nonetheless demands a closer look. To truly grasp the underlying motivations and anticipate Kazatomprom’s potential next steps, one must step back and examine the company’s broader strategic trajectory—beyond the surface of the August 22 production plan.

A DEEP DIVE INTO KAZATOMPROM’S INTERNAL STRATEGY

The shift in direction of the world’s largest uranium producer began with its 2018–2024 industrial strategy, in which the company decided to reverse course compared to previous years, when it had long flooded the market with uranium, focusing exclusively on extracted and sold volumes.

However, when the global energy landscape began to change, Kazatomprom realized that market conditions were evolving toward a structural uranium deficit destined to persist for decades. The conclusion was that it would be more rational to adopt a more optimal and conservative management of its resources—precisely what one would expect from a company aware of a future imbalance between supply and demand and of a consequent rise in prices.

The goal, therefore, became to reduce short-term production in order to maximize long-term profits, when the price of the commodity would inevitably increase. This vision was explicitly outlined in the 2018–2024 strategy and was subsequently implemented: “Since the implementation of the 2018–2028 Development Strategy, Kazatomprom has removed over 48,000 tonnes of uranium (124 Mln lbs) from primary global production, contributing to the recovery of the uranium market and to achieving a balance between supply and demand, while preserving uranium reserves for future needs and fostering sustainable long-term value.”1

This demonstrates how the idea had already been conceived eight years ago, when the company realized that flooding the market without discipline no longer made any economic sense. After experiencing the effects of a “volume over value” policy, Kazatomprom understood that such a strategy had not proved truly advantageous for anyone, since very few producers had managed to develop sustainably.

The result of that strategy was an extremely fragile market on the production side, in which Kazatomprom itself was never able to achieve profit margins comparable to those it earns today—and, above all, to those it will reach in the coming years. For years, the company effectively “spoiled” the utilities, granting them total bargaining power without constraints or limits, and allowing them to constantly hold the knife by the handle. This dynamic prevented not only Kazatomprom but the entire production sector from obtaining profits proportional to the real value of the commodity, almost eliminating the bargaining leverage of small and medium producers struggling to survive in a market environment strongly unfavorable to suppliers.

On January 15, 2025, Kazatomprom announced the approval of its new 2025–2034 development strategy. Although this update was received with little emphasis by the markets, it represents a crucial turning point for understanding the subsequent evolution of events. Its importance, however, was largely underestimated: from mid-October 2024, the market trend had taken on a flat trajectory, then gradually turned bearish, becoming strongly negative and reaching a low in April 2025.

This transition is essential to grasp one of the most significant characteristics not only of the uranium sector but of financial markets in general. When the price trend of a sector turns negative, positive news is systematically ignored, pushed into the background, or interpreted as irrelevant. It is a recurring and deeply irrational paradox: it is the price trend, more than the actual fundamentals, that drives the collective perception of an entire sector’s value.

During those months, the dominant perception among sector investors was that a deficit did not exist at all: it was believed that enormous quantities of uranium were ready to flood the market, that utilities were already fully covered until the next decade, and that, consequently, the entire narrative around a structural deficit was nothing more than an artificial construct fueled by so-called “pumpers,” that is, those who “pumped” a fundamental considered, in reality, to be without any concrete basis.

Meanwhile, however, the market was developing key, strongly bullish dynamics—completely invisible in the behavior of share

prices, which continued to fail to reflect the reality of the fundamentals.

And so, on January 15, 2025, Kazatomprom officially announced its development strategy for the new decade: the guiding principle would be supply discipline, meaning a preference for “value over volume.” On that occasion, the company opened the strategic document by recalling the success of its previous strategy, which had withdrawn 124 million pounds from the market from 2018 to 2024, thus further reinforcing the concept of disciplined resource management.

The goal is now to take the philosophy of resource optimization—introduced in the 2018–2025 plan—to a higher level, adapting it to a context in which the global nuclear renaissance is experiencing a much faster and more tangible acceleration than in the past decade. In this scenario, optimization can no longer be limited to production restraint; it must become a calibrated and scientifically planned strategy aimed at maximizing future profits with the available resources and those expected in the coming years.

A frequently overlooked but highly significant element is Kazakhstan’s declaration of its intention to develop its own domestic nuclear industry. The planned reactors—a number likely to increase in line with global nuclear expansion—would consume approximately 187 million pounds of uranium over their operational lifetime. Kazatomprom in fact specified, within its ten-year strategy, that part of its production could gradually be allocated to meet national demand.

It is important to remember that a significant share of Kazatomprom is state-owned. Consequently, it is more than reasonable to expect that the Kazakh government would want to secure uranium supply for its reactors at the lowest possible cost. And what could be more convenient than the price set by the company with the lowest production costs in the world, in which the State itself holds a substantial stake?

With the mid-2025 operational update, we arrive at the central point of the matter: the announcement of a cut in the 100% subsoil agreements, with planned production reduced from 85 to 77 million pounds, and the option to apply an additional 20% cut, down to a minimum production of 61.6 million pounds. In absolute terms, this means that between 8 and 23.4 million pounds of uranium could be removed from the market in 2026 — a potential cut of exceptional magnitude.

But why such a drastic decision? What is the real motivation behind such a strong signal sent by Kazatomprom to the market— and, in particular, to the utilities—at this specific historical moment? Could it simply be a move to keep uranium prices high?

The answer is no. The company has concluded that current market prices are profoundly—and I emphasize profoundly— misaligned with the industry environment that has consolidated and will continue to strengthen in the coming years.

To directly quote the company’s latest statement in the news released on August 22, 2025, and remove any room for interpretation: “However, the Company does not view the current market developments to be sufficient to return to the Company’s initial 100% levels at this time, which are now being decreased by roughly 8 million pounds, cutting about 5% of the world’s primary supply.”Only in this way can one fully appreciate why Kazatomprom believes that uranium prices do not in the slightest reflect the increasingly favorable structural conditions that now define this market.

1

https://www.kazatomprom.kz/en/media/view/announces_the_approval_of_its_updated_development_strategy_for_2025_2034

BUT WHAT IS THE ACTUALE STATE OF THE URANIUM MARKET? A NEW CALCULATION OF THE

UPDATED DEFICIT 2025-2040

The narrative is by now well known to anyone following the industry: the world is heading toward a projected uranium deficit that will become increasingly evident through 2040. The causes are multiple: the gradual depletion of output from existing mines, the enormous difficulty of bringing new projects into actual production, the delays and technical complexities in restarting sites that have been inactive for years—often unable to meet planned schedules and budgets.

To all this must be added a steadily growing global demand for nuclear energy, following a now clearly parabolic trajectory.

Looking at the long term, it becomes evident how much the picture has changed over the past two years, especially in light of the new data published by the World Nuclear Association (WNA) in the Nuclear Fuel Report released during the World Nuclear Symposium held in London from September 3 to 6 of this year.

In my master’s thesis, I sought to develop a demand-supply model capable of estimating, as realistically as possible, the raw uranium deficit from 2025 to 2040, using the most reliable tools and data available. Drawing on World Nuclear Association (WNA) data for the conversion of nuclear capacity into gigawatts and uranium consumption per reactor, and on the International Energy Agency’s (IEA) projections for global nuclear capacity through 2050, I constructed three growth scenarios—low, medium, and high—for the 2025–2040 period.

In my model, the low-growth scenario projected annual consumption of roughly 250 million pounds of uranium by 2040; the medium-growth scenario around 310 million; and the high-growth scenario approximately 351 million. However, the new WNA data, which extend demand projections through 2040, have substantially—and sharply—revised these estimates upward. In the updated outlook, the low-growth scenario for 2040 now forecasts around 280 million pounds per year, the reference case roughly 390 million, and the high-growth case an impressive 530 million pounds annually.

In other words, in just over a year, the market’s forward outlook has been completely redefined: the high-growth scenario of 2023 now shows a lower level of consumption than even the 2025 reference case, while today’s low-growth scenario matches the medium levels projected only two years ago.

This leap in magnitude highlights the extraordinary scope of the global nuclear industry’s expansion efforts, which have accelerated at an unprecedented pace over the past two years. In the charts that follow, the two datasets—the 2023 and the updated 2025 WNA projections—will be compared and cross-referenced with the prospective uranium mine production outlook through 2040.

It is important to emphasize that the columns representing prospective production have been deliberately constructed in an over-optimistic manner, precisely to yield results as conservative as possible relative to the real scenario: I preferred to

overestimate promised capacity in order to test how resilient the system remains under increasingly severe deficit conditions.

Confirmation of this choice comes from the comparison with the updated projections of the World Nuclear Association: the

productions I have drafted are indeed significantly higher than the WNA estimates. To account for the frequent discrepancies

between promised and actual production, my model incorporates two decisive scenarios: production at 90% and production

at 80% of what has been promised to the market.

These scenarios are not an academic exercise: historically and statistically, companies never achieve 100% of the resources

announced based on initial deposit studies. The actual percentage often falls well below 80% when deposits are still in the early stages of development, and even more so in pure exploration cases. For this reason, even the 80% scenario relative to promised production could actually be over-optimistic. I have nonetheless chosen to construct a conservatively designed model, providing the most solid possible base to start from and anticipating updates with more realistic data as they become available.

The model is structured as an intersection of multiple scenarios, allowing each reader to interpret the results according to their own view on risk and the likelihood of events. That said, I found that the 80% production scenario aligns more precisely with the WNA projections; for this reason, I consider it, among the three, the most realistic to use as an operational reference.

As for the three macro-demand scenarios—low, reference, and high—I leave it to the reader to assess which is most probable, always keeping in mind the significant upward revision of projections recorded over the past two years, which substantially modifies the relative probability of each.

A further methodological clarification: the comparison performed in the model exclusively contrasts the direct uranium demand from reactors with the prospective production of mines; secondary components of demand and supply are not considered here, in order to achieve a more direct analysis, less influenced by other exogenous factors that are difficult to predict.

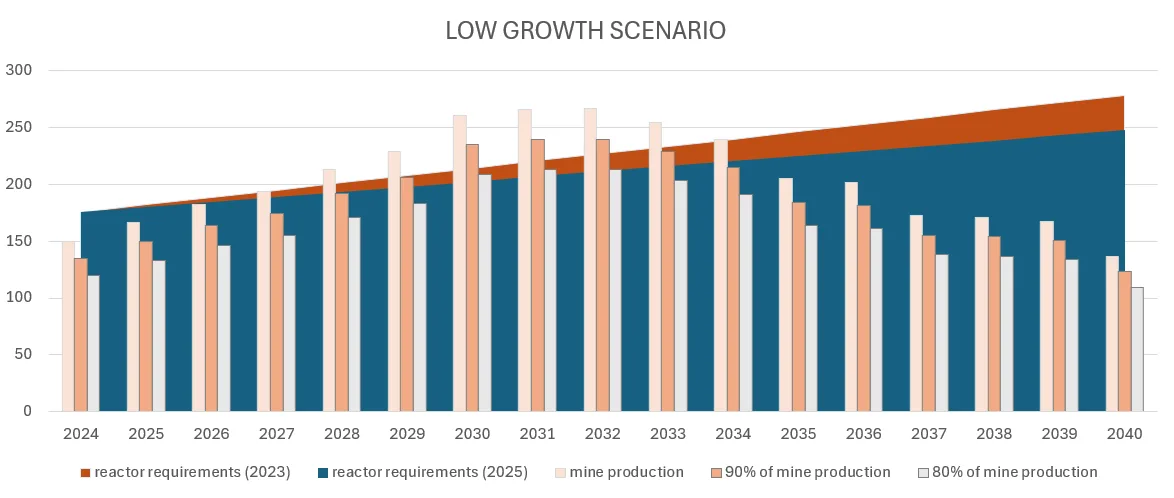

Below, I present the three scenarios with the two demand curves side by side—shown in blue and orange—and the columns of prospective production. The blue curve reports reactor requirements through 2040 based on 2023 data; the orange curve is based on the results of the WNA 2025 Nuclear Fuel Report. The columns, identical across the three scenarios, indicate the prospective production of mines in the three cases of 100%, 90%, and 80% of the production currently promised to the market.

LOW GROWTH SCENARIO

In the case of the low growth scenario, which represents the most conservative hypothesis of global nuclear expansion, the picture that emerges is already concerning in itself. Even in a context of slowed development and less aggressive demand, uranium supply struggles to keep pace.

Analyzing the charts, it is evident that only in the most optimistic case—assuming production at 100% of what has been promised to the market—does the supply curve manage, for a few years and for a limited period, to exceed the prospective demand of reactors. However, this hypothesis is little more than theoretical, almost utopian, as there are no historical precedents confirming the possibility of consistently maintaining production at the maximum declared level.

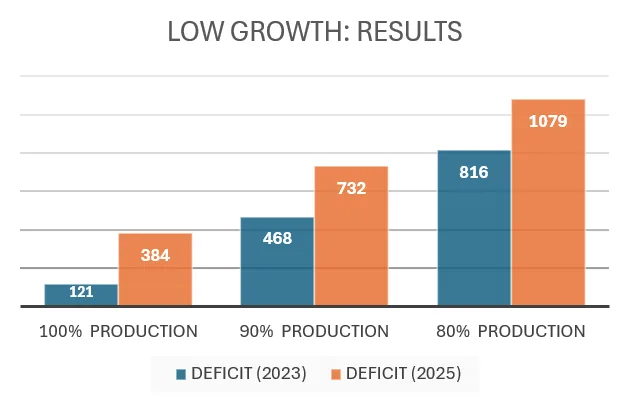

In the two more realistic scenarios, with production reduced to 90% and 80%, the result is unequivocal: demand almost always exceeds productive capacity. In some years the gap is minimal, but it grows rapidly over time, making it clear that even a scenario considered “prudent” shows a structural tendency toward deficit.

The average overall shortfall, according to the latest updated estimates, ranges from just under 400 million up to about 1

billion pounds through 2040, highlighting an average increase in the deficit of 55% compared to 2023 projections.

This dynamic suggests that, even with contained nuclear expansion, the uranium market will remain under big pressure, with an unstable supply-demand balance increasingly dependent on secondary sources or new, yet-to-be-confirmed mining discoveries. In short, the low growth scenario, which should have represented a safety point, actually reveals itself as a situation of structural tension in its own right.

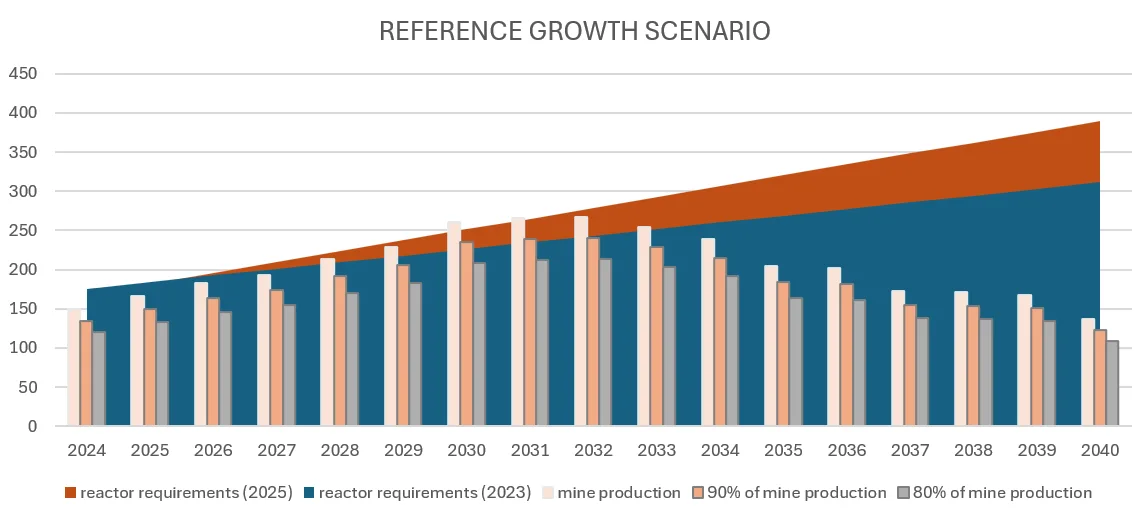

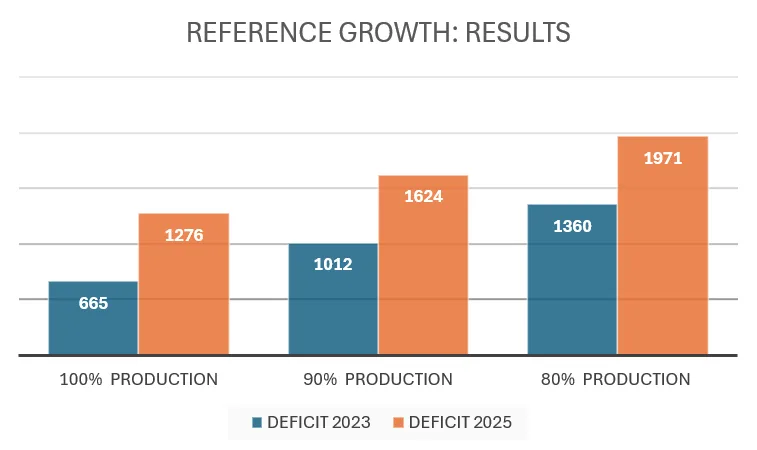

REFERENCE GROWTH SCENARIO

The medium growth scenario represents the development trajectory considered most probable, and precisely for this reason

its result carries crucial interpretative value.

Analyzing the data updated to 2025, the demand curve (in orange) not only consistently remains above the prospective production curve, but also shows a clear acceleration starting from 2030, when the new wave of nuclear capacity comes online globally.

In none of the years between 2025 and 2040 does supply significantly exceed demand, even in the most optimistic case of production at 100%. When this happens, it is a fleeting advantage, of only a few million pounds, limited to a single short period. In the more realistic scenarios, at 90% and 80%, the deficit rapidly widens, reaching dimensions of systemic significance.

By 2040, the average prospective deficit ranges from about 1.2 billion up to nearly 2 billion pounds, an increase of almost

65% compared to calculations based on 2023 data.

This scenario is particularly relevant because it represents, in probabilistic terms, the trajectory most consistent with current nuclear expansion plans and global energy policies. The emerging message is clear: even in a “balanced” situation, the system shows signs of rigidity and structural vulnerability, with demand growing faster than the mining industry can realistically supply. Pressure on prices and long-term supplies, in this context, is destined to become a dominant factor.

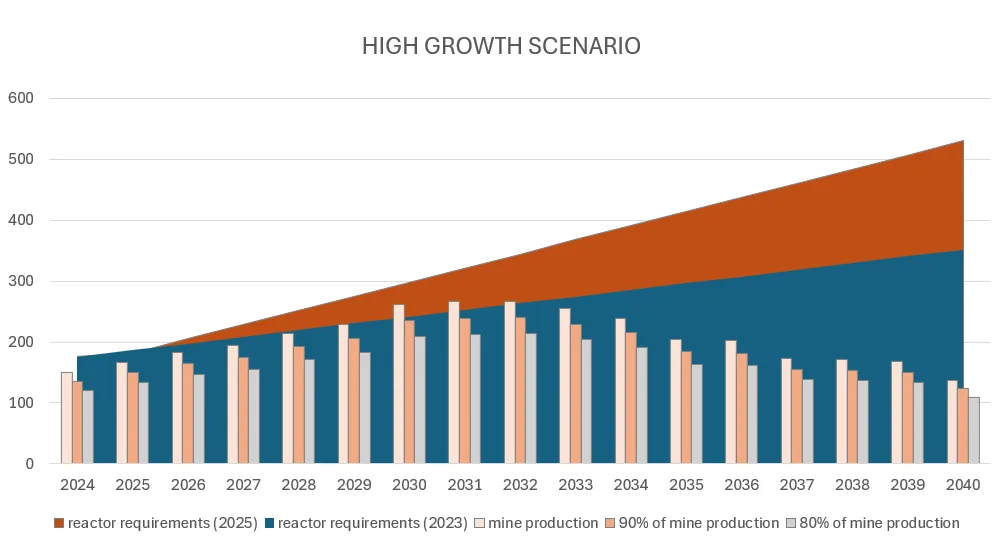

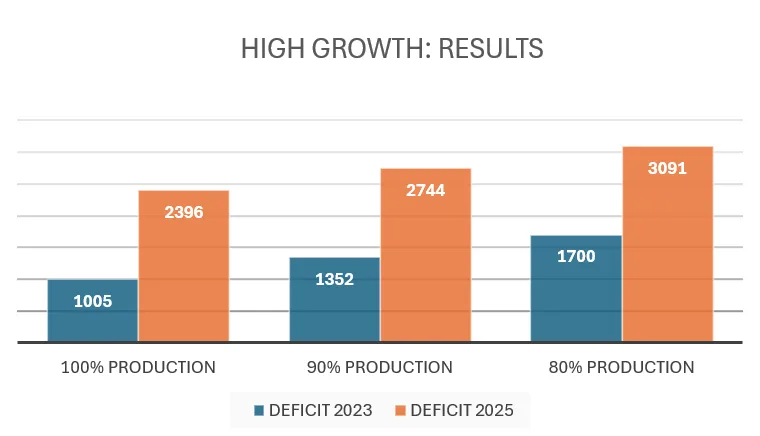

The high growth scenario, illustrated in the attached chart, is the one that best represents the magnitude of the ongoing transformation in the nuclear sector.

Here, the orange demand curve (updated to 2025) rises with an impressive slope, significantly surpassing the blue 2023 curve and clearly distancing itself from the prospective production bars already in the early years of the analyzed period. From 2025 onward, there is not a single year in which production, even assuming it at 100%, manages to match or exceed reactor demand: the gap is constant, wide, and continuously increasing.

The distance becomes abyssal in the more realistic cases of production at 90% and 80%, where the cumulative deficit reaches unprecedented proportions.

Projections indicate an unmet requirement ranging from 2.4 to 3 billion pounds of uranium by 2040, with an average increase of over 100% compared to previous estimates. This figure starkly illustrates the growing disproportion between global energy ambitions and the current actual extraction capacity of the mining sector.

In this scenario, the chart highlights the increasingly wide divergence between the exponential growth of reactor requirements and the slowness with which the market’s physical supply can respond. The demand curve rises visually like a wall, while the production bars remain fixed on an almost linear trajectory, a sign of an industry unable to expand at the same pace as global demand.

The result is a structural tension that cannot be filled even by assuming the entry into production of all currently planned projects. This scenario, although extreme, appears today less theoretical than it might have seemed just two years ago: the speed with which nuclear programs are announced, financed, and launched increasingly brings reality closer to the numbers of this simulation. In this context, the long-term deficit is no longer a remote risk, but a concrete and plausible trajectory.

CONCLUSIONS FROM THE CALCULATIONS AND GRAPHS

Each reader can draw their own conclusions in the face of these impressive results, which for those who have been investing in the sector for years — precisely due to the solidity of its fundamentals — are not entirely new, yet cannot fail to evoke emotions when observing the positive developments at a global level. These developments fuel an ever-increasing demand for nuclear energy and uranium, unequivocally reinforcing the fundamental reasons underlying this investment.

The model presented here aims to study the prospective situation based on current market conditions. Consequently, should prices in future years stabilize significantly above current levels, both in the spot and long-term markets, deposits that are not economically exploitable today could become so, offering a significant return to investors and incentivizing the construction of new mines. In such a case, an upward shift in the supply curve would be plausible, which otherwise, according to projections, shows a marked collapse starting from the mid-2030s.

However, it is essential to confront reality: the average estimated time required to build a mine ranges from ten to twenty years from the discovery of the deposit. This implies that the development of new deposits beyond those currently prospective would need to begin today in order to increase the supply curve when demand will be higher.

Since all current prospective deposits are already included in future production forecasts, it is logical to anticipate significant difficulties in raising the supply curve substantially. This does not, however, exclude the possibility that the stiffening of the very short-term curve, expected between 2028 and 2033, could take forms different from those outlined so far, with a more pronounced flattening of production and a central role played by Kazatomprom.

This article is intended to prompt the reader to reflect on the multiple signals provided by the world’s leading producer, Kazatomprom, whose actions largely determine the slope of the supply curve. The company appears inclined to preserve a portion of resources for the years of greatest need, deliberately flattening production and sacrificing a short-term production peak that could prove less convenient or not aligned with the new strategic vision that has been consolidating for several years and is increasingly defined.

In such a favorable and exponentially growing context, a similarly positive reaction of commodity prices, especially in the long-term market, would have been natural to expect. However, such a response has not yet materialized.

IS IT TRULY CORRECT THAT THE PRICE HAS NOT ALIGNED WITH THE IMPROVEMENT IN THIS MARKET’S FUNDAMENTALS?

It is crucial to understand that all these positive developments in the global nuclear industry, which have led to a significant upward revision of uranium demand estimates for reactors through 2040, have not occurred during the recent months of appreciation in mining company stocks or slight growth in the commodity price.

The policies of constructing new reactors, extending the lifespan of existing reactors, and the reversal by nearly all states that had imposed bans on nuclear energy have developed gradually and steadily over recent years, even during periods of sharp price declines.

On the supply side, over the years we have witnessed continuous and repeated delays in numerous projects, demonstrating to the market the impossibility of producing within the planned timelines and budgets.

Despite this slow but steady improvement in fundamentals, the spot price of uranium has not reflected it at all; in fact, for

over a year and a half, it maintained a downward trend. It is clear that the spot market is extremely illiquid, subject to sudden increases but also steep drops, driven primarily by a few transactions carried out by traders rather than by utilities, which prefer to secure supply through long-term contracts to ensure stable provision for their reactors.

Even the long-term market has not shown a significant realignment with the growing fundamentals: for about a year and a half, the price remained frozen between $80 and $81, despite a substantial increase in the production incentive price due to exponentially rising development and production costs. It is therefore evident that the stagnant view of the long-term market was supported by a prolonged period of inactivity by utilities, many of which were reluctant to pay prices higher than the historical average they had grown accustomed to over the past fifteen years.

After a long period in which uranium supply was always guaranteed without difficulty—both thanks to Kazatomprom’s massive production flooding the market with enormous quantities of pounds, and through nuclear warhead dismantling programs such as Megatons to Megawatts, which introduced tens of millions of pounds of uranium annually—the shock caused by rising prices froze many buyers of raw uranium.

Utilities were also able to gain contractual leverage by relying on the support of a sharply declining spot price and an extremely weak production market, in which many operators struggled for over a year and a half to survive and secure the necessary capital to overcome the critical phase.

For this reason, on several occasions, many producers were forced to enter pre-supply contracts even before actually entering production, at prices lower than the current commodity price, just to raise the capital essential for their survival.

Others, instead, had to sell pounds on the spot market to obtain immediate liquidity, thus contributing to the downward cycle of the price.

This was compounded by the impact of sanctions on the ban of Russian uranium imports, which, controlling a significant share of production in the enrichment and conversion phases, created a bottleneck in the nuclear fuel production chain.

Utilities therefore had to focus their attention on these two phases, postponing negotiation of the first, raw uranium, which, however, is also the last to be traded in the nuclear fuel procurement cycle.

Consequently, the quantity of raw uranium contracted on the long-term market in the past year and a half was significantly lower than the annual needs of reactors. The result was a market where, despite clear positive signals from prospective nuclear energy demand and the evident difficulties of producers in increasing output, prices experienced a downward phase that persisted for over a year. The spot price, from the highs of $106 per pound in January 2024, fell to lows of $64 per pound in March 2025, rising today to $82, while the long-term price remained stable and flat for more than a year and a half.

HOW DID THE DOWNWARD PRICE DYNAMICS AFFECT KAZATOMPROM’S PROFITABILITY?

The recent price action had a significant impact on Kazatomprom’s realized price, which the company has repeatedly emphasized, as many of its contracts are effectively anchored to the spot price, directly influencing the effective price obtained from uranium sales.

The price realized by the company, from a $66.19 average in June 2024, fell to $58.54 on average in the year to June 2025, registering a substantial decrease of over 12%.

An equally crucial aspect concerns the total costs faced by the mining company. The AISC (All-in Sustaining Cash Cost) increased from an average of $28.10 in June 2024 to $30.81 in June 2025, a significant rise of 10%. This increase was justified by the company with the rise of the MET tax rate for 2025 and the increase in the cost of sulfuric acid, a key component in the ISR process for uranium extraction.

It is also natural to consider how sanctions, the obligation to use alternative routes, and the partial closure of more favorable markets have contributed both to cost increases and to the reduction in the realized price.

Consequently, the profit margin between the average price realized from raw uranium sales and total costs fell from $38.09 in June 2024 to $27.73 in June 2025, marking a stunning decrease of 27%!

It is clear and natural that, combining the concept of production discipline with the decline in market price, the low activity in the long-term market by utilities, and the rise in costs, Kazatomprom decided to confirm its supply discipline policy through a significant cut in the 2026 outlook.

WHAT TO EXPECT FROM KAP’S NEXT STEPS IN THE SHORT TERM BUT ALSO IN THE MEDIUM/LONG TERM?

A key element justifying the resource optimization and the planned production reduction for 2026 is the shortage of sulfuric acid affecting Kazakhstan and, consequently, Kazatomprom itself. The scarcity of this raw material, primarily destined for the country’s agricultural sector, has caused a significant cost increase, compressing the company’s profitability.

To address the issue, Kazatomprom has started construction of a large internal sulfuric acid production plant, which, however, even if completed on schedule, will not become operational before mid 2027. Pushing production to the maximum before this plant is available would mean “wasting” resources during a period of lower profitability than would be possible once the internal plant is operational, which would significantly reduce extraction costs. This represents the main short-term driver for the production reduction.

However, there are reasons to suggest that Kazatomprom may adopt an even more sophisticated resource optimization strategy, extended to the medium and long term, well beyond what has been communicated to the market so far. A critical factor is the significant depletion of resources expected from the mid-2035 period. The charts published by the company show a drastic decline in production starting from that year, highlighting relevant future problems if new resources are not discovered through robust exploration activity.

In summary, Kazatomprom’s strategy may not be limited to a simple short-term tactical response: it aims to preserve and manage resources optimally, balancing immediate profitability and future production sustainability, in anticipation of the drastic drop in resources expected in the following years.

Assuming that the increase in uranium prices will certainly occur and that its magnitude will depend on the market environment, it is evident that Kazatomprom could choose to partially flatten the production curve, sacrificing part of the short-term profit to benefit from much higher prices in the mid-2030s, leveraging mines already discovered and currently among the most efficient and low-cost in the global uranium landscape.

It is easy to imagine how extremely advantageous it could be for the company to bring already substantially infrastructured mines into production in the near future, when the development costs will be significantly higher than the current one. This aspect, although often overlooked, has been emphasized by industry experts such as Rick Rule.

We are in a historical period in which inflation for mining companies hovers around 9% to 10% per year compounded.

Considering the time required to plan and build new mines, the future costs of mines in the next decade will be enormously higher compared to those already existing. This, in turn, will push up the incentive price of the raw material, resulting in an exponential increase in the profitability of future production extracted from mines whose main costs have already been incurred today.

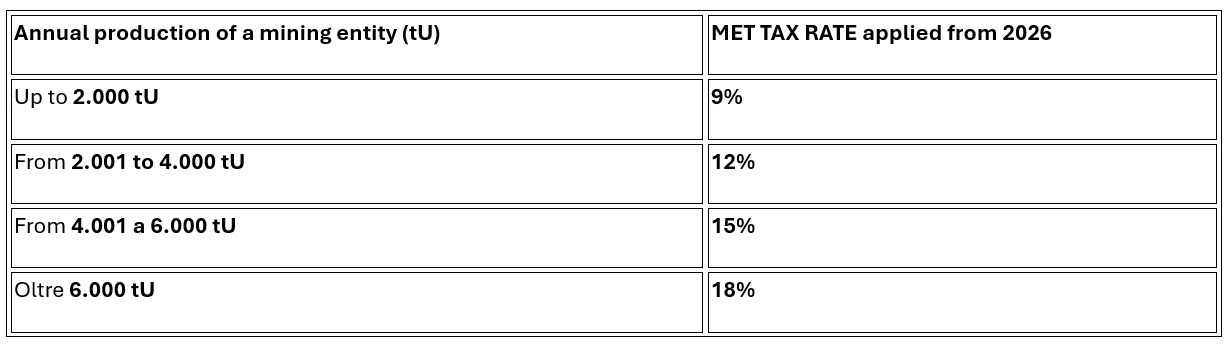

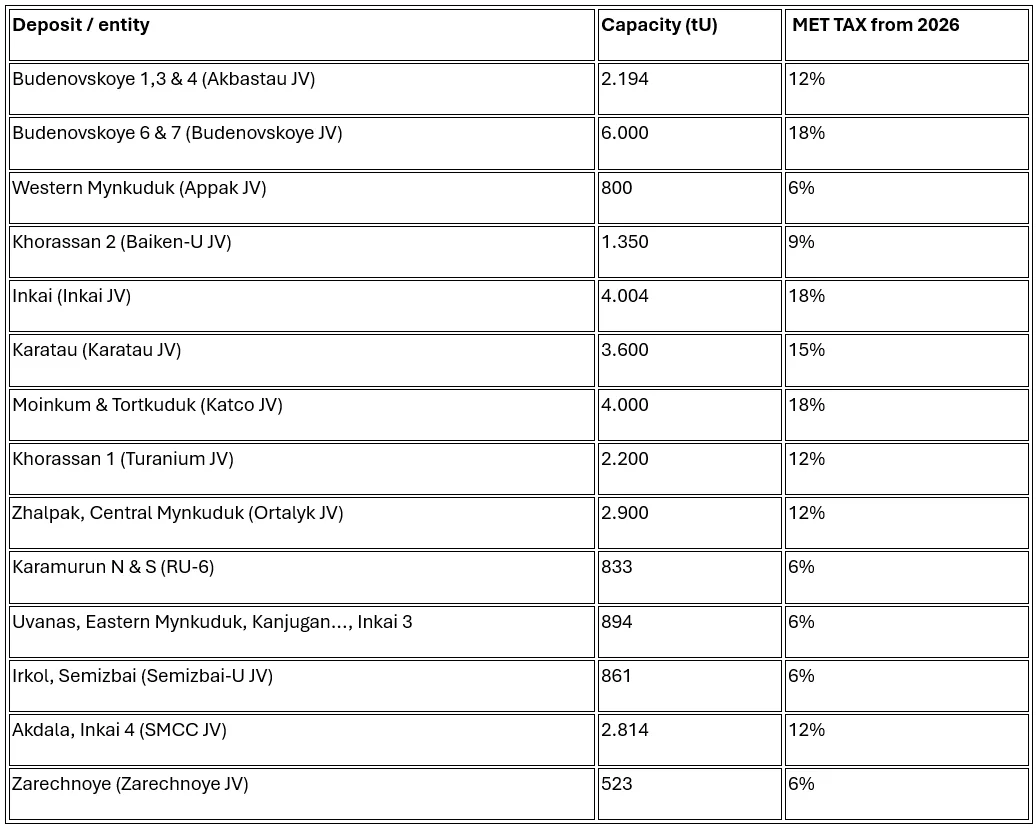

Another critical factor, often overlooked in discussions about uranium production in articles and on social media, is the strategic shift in taxation implemented by the government of Kazakhstan in July 2024. The tax rate, which started this year at 6% and will rise to 9% in 2025, is set to increase significantly from 2026 onward. The new framework is progressive, applied according to the production output of each mining entity in the country, and reaches a maximum of 18%, creating strong incentives for production optimization at the entity level.

Kazatomprom’s corporate structure is far from straightforward. The company operates as a “corporate box” comprising multiple legally distinct entities, each linked to a specific mining project, yet all controlled by the parent company. This setup allows the company to strategically manage both production and taxation across its portfolio, balancing short-term cash flow and long-term resource preservation.

To illustrate the implications, the following section presents a detailed table showing the progressive tax schedule coming into effect at the beginning of 2026, alongside the current production capacities of all mining entities within Kazatomprom.

This data highlights how the company could deliberately modulate annual output across different mines, minimizing tax

burdens while maximizing profitability, and ensuring that the most cost-efficient assets are prioritized in periods of tighter

margins.

Taken together with factors such as production discipline, rising operating costs, and resource management strategy, it becomes increasingly evident that Kazatomprom may deliberately flatten its production curve in the coming years. A steady near-term output could be maintained, avoiding short-term spikes, with a controlled decline expected after the mid-2030s, aligned with resource availability and market conditions.

This analysis is crucial to understanding how the uranium market could evolve over the next 15–20 years, providing a solid

foundation for a robust, strategically managed sector that benefits both the company and long-term investors, while

highlighting the increasing role of taxation and entity-level planning in shaping global uranium supply.

HOW TO NAVIGATE THIS PERIOD OF GROWING OPTIMISM WITHOUT GETTING BURNED?

It is evident that the current market situation shows an increasingly growing optimism among sector investors. We are not yet at euphoria levels, as the wounds left by the shocks of 2021 and 2023 are still present, but it is undeniable that the current reality exhibits the first signs of unconditional investor positivity.

As has happened in the past, during periods of rising stock prices, the narrative tends to become increasingly enthusiastic, leading almost every new piece of news related to the sector to be interpreted as an additional driver for price increases.

Conversely, during periods of weakness—such as the last one—positive news is ignored, while any potentially negative event is amplified and becomes a reason to justify further declines.

The truth is that one could imagine a chart where the line representing the sector’s fundamentals grows slowly but steadily, while the sentiment line fluctuates violently, significantly exceeding the average during euphoric moments and falling well below it during periods of panic.

Evidence that fundamentals move steadily, albeit very slowly, comes from the testimonies of experts and industry insiders who, over 20, 30, or even 50 years, have described the extended nature of nuclear industry cycles. A single fuel contracting cycle can take several years, while the development of a deposit, from discovery to full operation, can take almost a quarter of a person’s life.

Consider that the strategic adaptation and changes at Kazatomprom took seven years to fully manifest; it is therefore reasonable to expect that new developments will also require time before being fully reflected in the market. Similarly, the price of uranium has remained stable for over a year and a half despite favorable market conditions—further evidence that the current rise in stocks already partially reflects an imminent increase in the price of the commodity.

It’s clear that improvements, both in terms of demand and supply, are indeed underway, accompanied by a modest but noticeable acceleration. Yet, it remains crucial to stay vigilant against overheating optimism, avoiding the temptation to believe one is witnessing a “train that will never pass again.” The history of the uranium market has repeatedly shown that the train always returns, often multiple times. The key takeaway is to recognize when the short-term sentiment curve excessively exceeds the slow but steady improvement in fundamentals—and consequently the intrinsic value of the companies of interest.

A clear certainty emerges from the announcement of the world’s leading producer, which declared the end of the era of “cheap pounds”; this statement is mathematically true. The significant increase in costs faced by the world’s most efficient producer demonstrates how much higher costs will be for all other, considerably less efficient operators. Therefore, it is reasonable to expect that these favorable market conditions will eventually be reflected in the price of uranium—both in the short and long term—without presuming to predict the exact timing.

Ultimately, the only certainty is the need to continue analyzing rigorously, through in-depth analisys, the conditions that make a sustainable, long-term bullish cycle possible. The conclusion is clear: careful, evidence-based observation and strategic foresight remain essential for navigating and capitalizing on the evolving uranium market.