Presented company is our client!

Marc Henderson, CEO of Laramide Resources Ltd. (TSX: LAM; OTCQX: LMRXF, ASX: LAM), provided an in-depth look into the company’s strategic decisions, project advancements, and the broader uranium market dynamics. As of February 4, 2026, with uranium spot prices hovering around $92 per pound after a brief surge above $100, Laramide’s focus on U.S. and Australian assets positions it to capitalize on growing demand for secure, Western-sourced uranium. This article expands on the interview to highlight Laramide’s path forward in a market projected to double supply needs by 2040.

Exiting Kazakhstan: A Strategic Retreat from Greenfield Exploration

Laramide’s decision to exit its Kazakhstan exploration assets, announced on January 20, 2026, marks a significant pivot for the company. Henderson explained that the move was driven by evolving government policies that effectively nationalized the exploration phase of uranium projects. Under new Subsoil Use laws formalized in December 2025, foreign entities like Laramide would retain only 10–25% ownership in any discoveries, with the state claiming 75–90%. Initially drawn to Kazakhstan for its geological potential -- including, adjoining major trends and producers like Kazatomprom, -- Laramide entered with eyes open, expecting partnerships similar to those that kickstarted the country’s ISR (In-Situ Recovery) production boom. However, as Henderson noted, “they decided that they really want to control their outcome completely.” Despite positive experiences with local authorities, bureaucracy, and expertise—praising the country’s ISR prowess honed from Soviet-era endowments—the economics no longer justified the investment for shareholders.This exit underscores broader supply risks from Kazakhstan, the world’s largest uranium producer. With production at around 70 million pounds annually and geopolitical positioning between Russia and China, Western reliance on Kazakh supply could face constraints, amplifying the need for diversified sources.

Accelerating U.S. Assets: Churchrock and the Push for Domestic Production

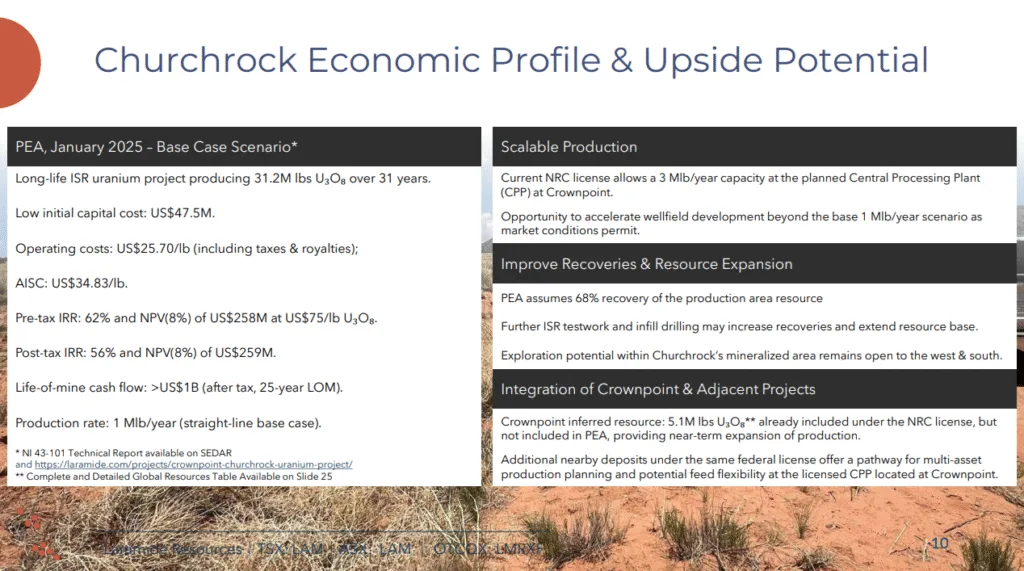

With Kazakhstan behind it, Laramide is ramping up efforts on its U.S. portfolio, particularly the Churchrock-Crownpoint ISR project in New Mexico. Henderson emphasized that Churchrock, advancing under the federal FAST-41 permitting process, is on track for potential production by Q2 2027. This timeline aligns with U.S. government priorities for domestic uranium security, especially amid heavy import dependence—domestic production remains only a small fraction of total U.S. reactor requirements.Churchrock stands out for its regulatory readiness: It holds an existing NRC (Nuclear Regulatory Commission) license, allowing for phased development starting at 1 million pounds per year, scaling to 3 million via a licensed processing plant at Crownpoint. Combined, the projects host about 56 million pounds of resources (*Inferred), with exploration upside. Henderson highlighted milestones for investors: permitting progress, drilling data later in 2026, and groundwork for well fields. “We’re going to pivot back hard,” he said, noting the project’s already robust economics improve with uranium prices: for instance at today's price U₃O₈ $91.80/lb, the after-tax NPV(8) $423.8mmOther U.S. assets include La Jara Mesa in New Mexico (hard-rock, FAST-41 permitted) and La Sal in Utah (fully permitted underground project near Energy Fuels’ White Mesa Mill). Henderson discussed challenges for hard-rock projects, like limited milling capacity, but advocated for new mills to unlock potential. Crownpoint, while deeper and slated for later integration (year 10+), will host the processing plant, leveraging historical shafts from the 1970s.This focus is timely given U.S. vulnerabilities: Canada, historically the top foreign supplier of uranium to U.S. utilities, is diversifying trade under Prime Minister Mark Carney, including energy opportunities with China. This could reduce volumes available to the U.S., heightening Churchrock’s role in bolstering domestic supply.

Australian Opportunities: Westmoreland, Murphy, and Exploration Upside

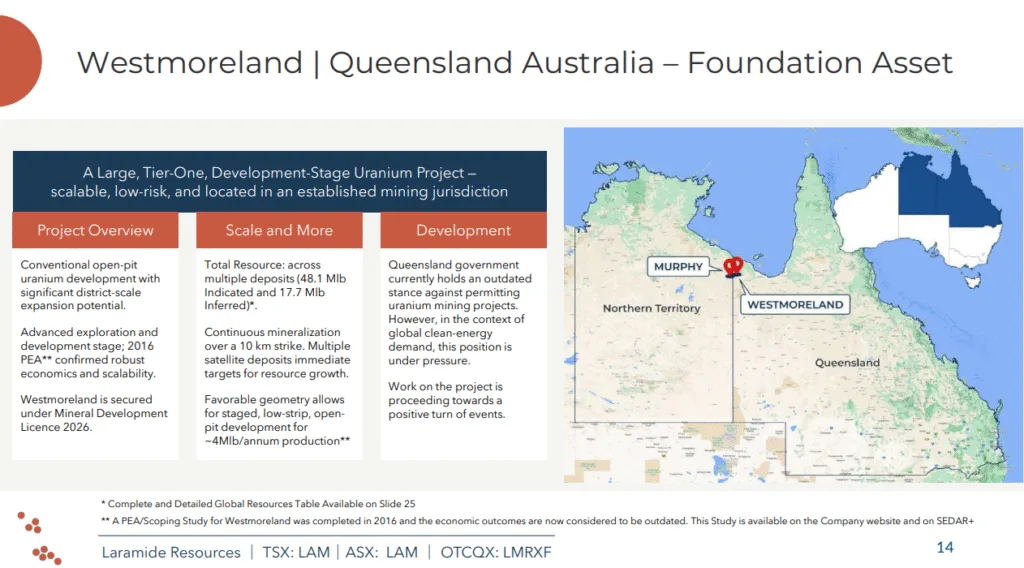

In Australia, Laramide’s Westmoreland project in Queensland boasts around 65 million pounds of resources, with potential to expand to 80–90 million. Henderson outlined plans for aggressive exploration in 2026, including drilling from mid-May to November, targeting high-impact zones. An updated economic study—last done in 2016—is forthcoming, projecting 5–6 million pounds annual capacity at higher resources.The adjacent Murphy project in the Northern Territory adds scale, with multiple targets and adjacency to DevEx Resources’ activities. Henderson sees Australia as a future greenfield hotspot, especially as policies evolve to support uranium amid global demand. Boss Energy holds a 20% stake in Laramide, acquired at a favorable price, and relations remain strong despite Boss’s production revisions. Henderson hinted at potential future developments, noting Boss’s technical capability and interest in Westmoreland as a supply source.

Uranium Market Dynamics: Supply Deficits and Price Sensitivity

Henderson painted a bullish picture for uranium, driven by demand projections from 180 million pounds annually to nearly 400 million by 2040, per World Nuclear Association estimates. “2040 in the uranium business is tomorrow,” he quipped. With deficits akin to silver’s recent run—but less elastic supply—prices could sustain above $100, making marginal projects viable.Laramide’s projects are highly sensitive to price: Higher revenues enhance economics, especially for ISR like Churchrock. Global concentration—Kazakhstan at roughly 40% of production, Athabasca Basin next—highlights risks, with replacements needed by 2040. Henderson foresees behavioral shifts: utilities “crying uncle” on prices, or end-users like tech giants investing directly. Nuclear’s role in data centers and carbon-free energy amplifies this, with uranium equities benefiting from passive ETF flows.Recent stock performance supports this: LAM shares hit a 52-week high of C$0.91 on January 29, 2026, up over 50% year-to-date, partly from ETF reweightings and sector momentum.

Share Structure, Relations, and Future News Flow

Boss Energy’s 20% stake remains stable, with Henderson praising their candor on ISR startup challenges. Laramide’s market cap reflects undervaluation, but pivots to core assets could unlock value. Investors can expect permitting updates, Australian drilling results, an updated Westmoreland study, and U.S. groundwork in 2026. As Henderson noted, “We’re going to embrace the optionality,” positioning Laramide for an “inevitable” supply crunch.In summary, Laramide’s strategic exit from Kazakhstan refocuses resources on advanced U.S. and Australian projects, aligning with Western supply security needs. Amid shifting trade landscapes and surging demand, the company is poised to contribute meaningfully to the uranium renaissance.

WATCH THE INTERVIEW: